Are you earning well but feeling financially strained? You may be falling into traps that drain your finances. Discover how saying "no" can help you keep your hard-earned money.

Are you earning well but feeling financially strained? You may be falling into traps that drain your finances. Discover how saying "no" can help you keep your hard-earned money.

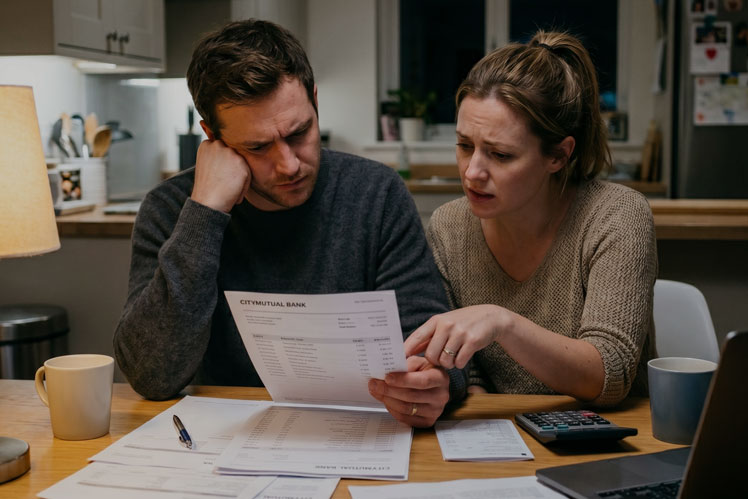

Many people struggle with retirement planning and often wait for life events to take action. Despite clear steps like recording expenses and saving, few Canadians follow through. A recent survey revealed that couples frequently disagree about their retirement plans.

Navigating severance packages can be daunting, especially in today's unpredictable job market. With the right tax planning strategies, you can maximize your severance pay and retain more of your money.

Have you ever stopped to think about the sneaky little dance happening in your wallet every single day? It’s a constant tango between inflation and purchasing power. Understanding purchasing power is crucial for achieving true financial independence.

Many people assume their employer's group coverage will meet their needs. However, as Sally, Peter, and Steve found out, relying solely on it can lead to serious issues. From inadequate life insurance to denied disability claims, group plans can be unpredictable.

Are you prepared to make your retirement savings last? With longer life expectancies, it's vital to rethink your investment management. The traditional approach of shifting everything to fixed-income options may not be effective.